Franchisors

Centralize royalties, recoveries, multi-entity accounting, payment orchestration, and operational visibility without scattering the workflow across separate vendor silos.

Digital sovereignty for operators

RAAMP gives franchisors, tenants, and commercial property owners a way out of rented dependency. Own your operations again with a private hosted instance now, or a perpetual source-code path when you are ready.

You should not be owned by your software. We give you a way out.

Own your operations again.

Private infrastructure, not rented leverage

Built for the people carrying the load

RAAMP is not another generic dashboard. It is operational infrastructure designed to help real teams run franchising workflows, tenant relationships, accounting, payments, files, and signatures in one controlled system.

Centralize royalties, recoveries, multi-entity accounting, payment orchestration, and operational visibility without scattering the workflow across separate vendor silos.

Give tenants a cleaner experience for payments, documents, signatures, notices, and shared operational history while keeping the system anchored to your team and your process.

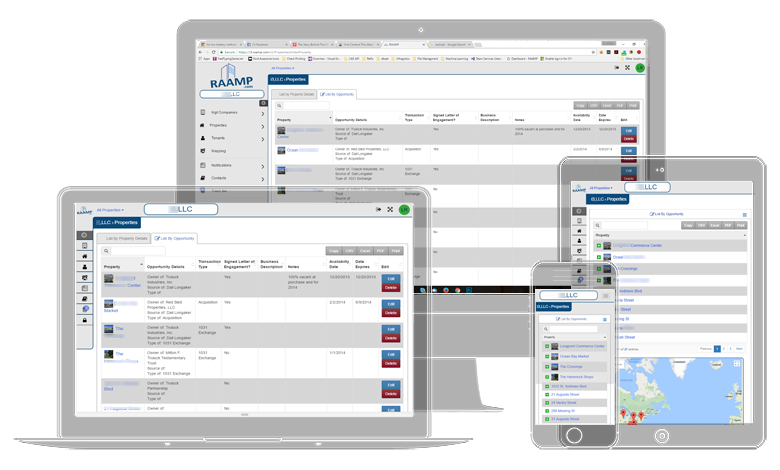

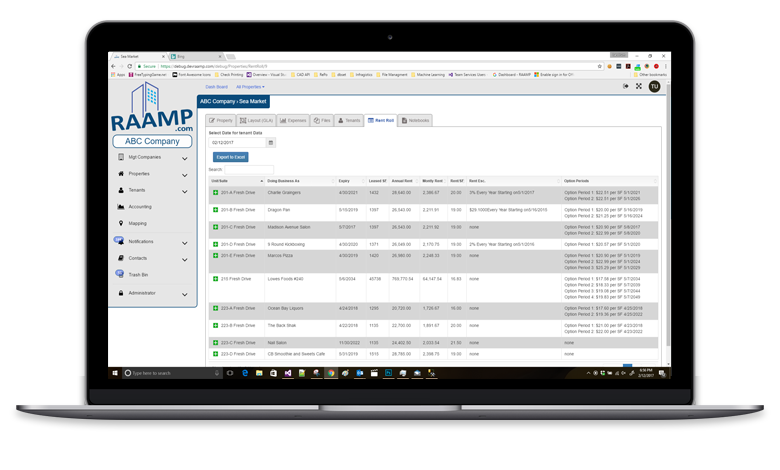

Manage leases, entities, accounting, files, and mission-critical dates from a platform that understands the realities of complex ownership structures and commercial operations.

Platform and partnerships

RAAMP is differentiated because it already combines the core pieces operators normally have to stitch together from multiple vendors and multiple subscriptions, and it deploys them solely on the Microsoft stack.

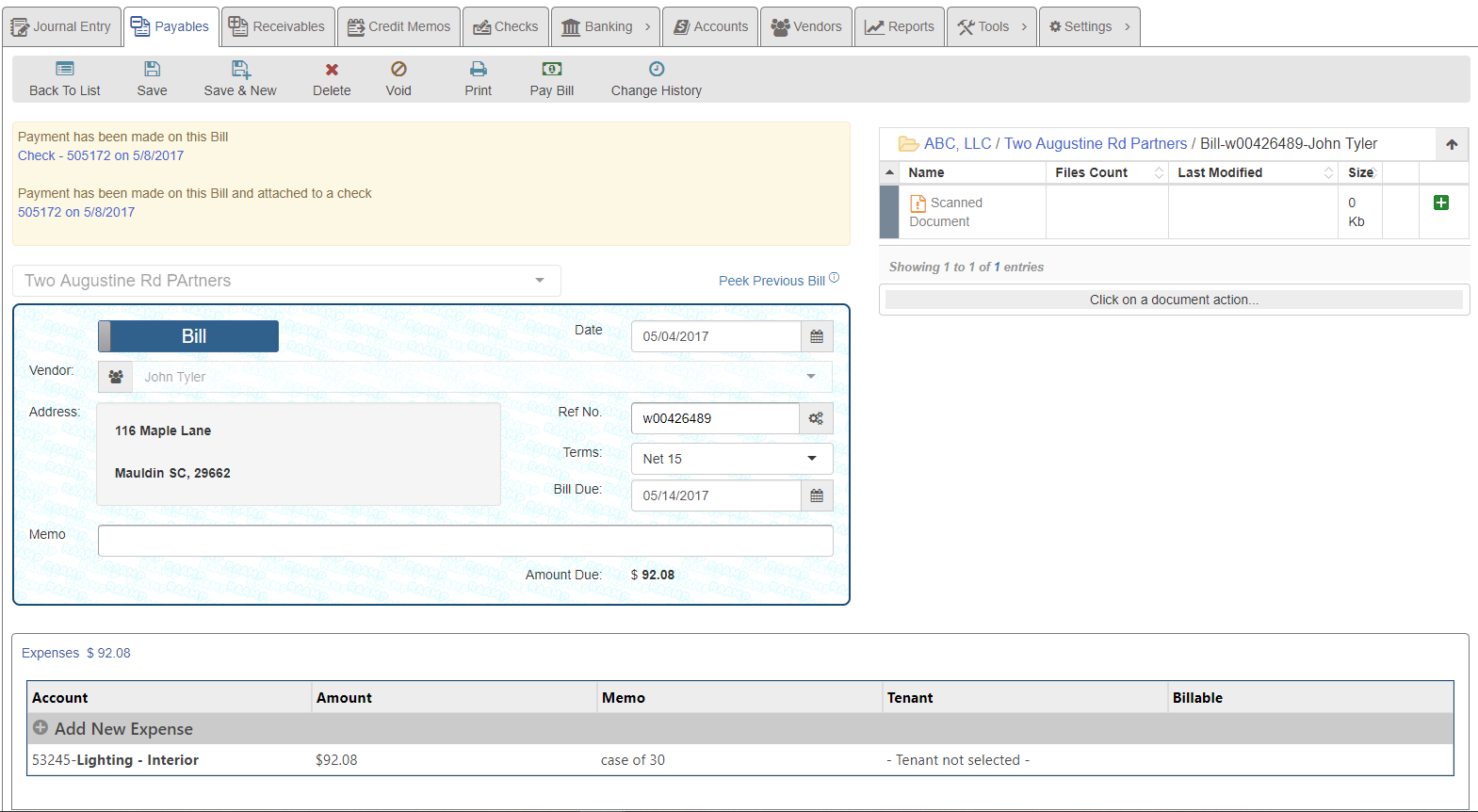

Collect and manage payments inside the system instead of handing off critical cashflow workflows to disconnected tools.

Run bill pay through a workflow that is already aligned to the accounting and approval structure in RAAMP and supported on the same foundation.

Use a seamless integration with Tax1099.com so vendor data, 1099 workflows, and year-end filing stay connected to the accounting structure already living in RAAMP.

Move signatures directly through the platform so execution does not live in a separate operational universe or outside the your ERP deployment.

Use AI where it belongs: inside the operating system, close to the documents, data, and workflows your team already runs on a codebase built for repeatability.

Support tenant, landlord, and franchisee call-center workflows on Twilio Flex with SSO and record-linked context already living inside RAAMP.

Handle the real structure of your business instead of flattening everything into a subscription-friendly compromise.

AI built on repeatability

RAAMP has been built for more than a decade with standardized features, optimized code, and repeatable engineering patterns. That matters now because AI is most valuable when it can operate inside a system that already has structure instead of fighting chaos.

The developers built RAAMP on repeatability so maintenance, improvement, and new work start from a standardized base instead of a blank page.

In the ownership model, your team can use vibe coding agents powered by the latest Codex models to help maintain, improve, and operate RAAMP with the code on your side.

Ownership is not limited to using RAAMP as delivered. You can write your own software on top of the platform, and we can show your team how to do it responsibly.

RAAMP is built and deployed solely on the Microsoft stack, giving AI, integrations, and operational workflows one consistent technical ai foundation.

What that looks like in practice

The platform is already standardized and operationally ready. You are not buying an idea deck. You are buying a running ERP that is prepared for customization and control.

Run real multi-entity accounting without jumping between disconnected files, subscriptions, or approval chains.

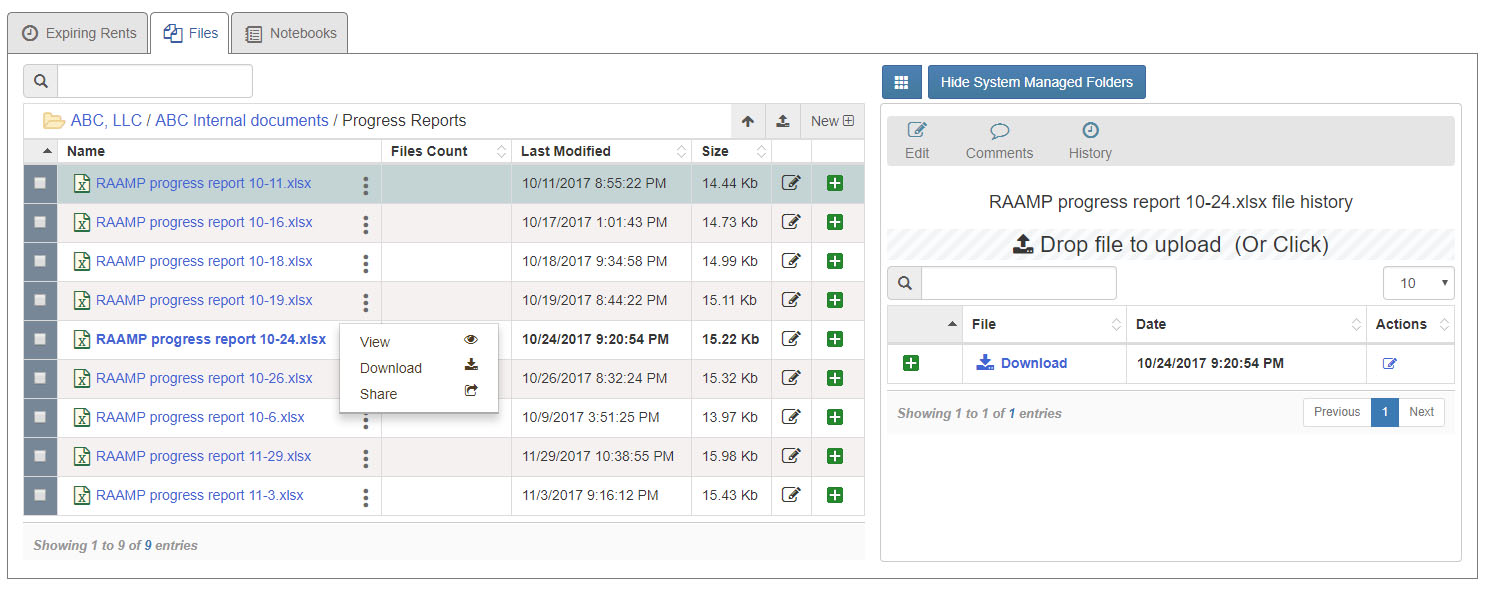

Keep documents, revision history, comments, and operational context in one place so your system remembers what your people already know.

Start with a hosted private instance, then move toward total ownership when you want the code and the leverage on your side.

Qualitative comparison

Those systems may fit parts of the job, but the software company still owns the roadmap, the infrastructure decisions, and the pace of change. RAAMP is about changing the balance of power.

R365

Still a rented roadmap. RAAMP is positioned as your operating infrastructure, not just another monthly layer.

Yardi

RAAMP pushes control back toward the operator with private instances now and full ownership later.

MRI

RAAMP's difference is not feature theater. It is the option to become the owner of the system itself.

QuickBooks Enterprise

RAAMP combines accounting, payment flows, signatures, files, tenants, and operational history in one environment.

Two ways out

You are not trading one lock-in for another. You are choosing how quickly to move from operational control into full ownership.

Hosted RAAMP

Private hosted RAAMP instance for teams that want control now without standing up infrastructure on day one.

Perpetual ownership

Payment terms available. Own the source code, host it your way, resell it if you want to, and stop rebuying the license.